₹12.2 lakh crore allocation, PPP risk coverage and ₹50,000+ crore REIT redevelopment pipeline set to drive 8–12% equipment growth in FY26.

Record capex, Risk Guarantee Fund, CPSE REITs and CIE scheme create a 3-5 year tender pipeline for EPC contractors, OEMs and procurement managers.

EXECUTIVE SUMMARY

Finance Minister Nirmala Sitharaman announced â‚ą12.2 lakh crore capex for FY27 (+9% YoY), 3.1% GDP allocation. Under the Construction & Real Estate sector, Pepagora analysis identifies immediate tender opportunities across rail (â‚ą2.62L cr), roads (â‚ą2.78L cr) and urban infra (â‚ą1.12L cr). The budget also reinforces the agenda supported by Shri H. D. Kumaraswamy, Minister of Heavy Industries, to strengthen domestic manufacturing through focused equipment sector interventions.

3 Game-Changers for Construction

- Risk Guarantee Fund – De-risks ₹3–5 lakh crore PPP projects by improving credit quality and unlocking stalled infrastructure pipelines.

- CPSE REITs – Enable ₹50,000+ crore worth of redevelopment contracts through asset monetisation and Grade-A commercial upgrades.

- CIE Scheme – ₹200 crore allocation to promote construction equipment localisation, strengthening domestic manufacturing and reducing import dependence.

CAPEX BREAKDOWN

India infrastructure growth shows strong capital dependence supported by a six times increase in capital expenditure since FY15, rising from â‚ą2 lakh crore to â‚ą12.2 lakh crore. National Highways account for â‚ą2.78 lakh crore driving demand for asphalt pavers and motor graders, while Indian Railways with â‚ą2.62 lakh crore investment supports rail tampers and ballast regulators. Urban Development contributes â‚ą1.12 lakh crore, strengthening the need for tower cranes and concrete pumps across expanding city projects.

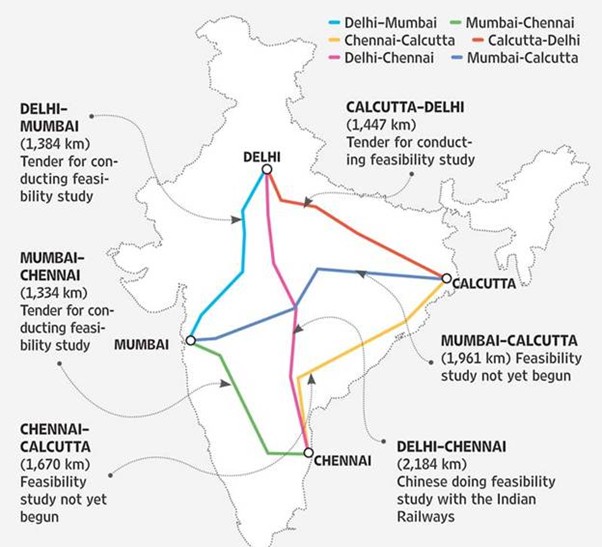

7 High-Speed Rail Corridors (Mumbai-Pune, Delhi-Varanasi + 4 others): 2,500+ kms earthmoving demand.

TENDER OPPORTUNITIES

Risk Guarantee Fund = HAM Revival

The introduction of the Risk Guarantee Fund is accelerating the revival of the Hybrid Annuity Model (HAM). With 10–20% construction risk coverage, several BB-rated projects are now being upgraded to investment-grade, improving financing confidence and project viability. The immediate impact is visible in the rise of HAM awards to 240 km per month, compared to 120 km in FY24. Pepagora is currently tracking 52 live HAM tenders worth ₹28,000 crore, indicating a strong execution pipeline in the infrastructure sector.

CPSE REIT Pipeline

A ₹50,000–75,000 crore CPSE asset monetization pipeline is unlocking Grade-A redevelopment opportunities. This includes large-scale office retrofits such as MEP upgrades and seismic strengthening, transit-oriented development (TOD) projects around rail corridors, and industrial park conversions. These initiatives are expected to drive sustained demand across construction materials, real estate services, and heavy equipment segments.

Tier-2/3 Urban Shift

The development of City Economic Regions is accelerating growth across Tier-2 and Tier-3 cities, with 25–30 clusters valued at approximately ₹5,000 crore each. Target cities including Coimbatore, Surat, Varanasi, and Visakhapatnam are emerging as high-growth hubs. This shift is projected to increase demand for construction and real estate equipment, particularly 15–25T excavators and compact machinery, as infrastructure activity expands beyond major metropolitan areas.

cranes.

EQUIPMENT FORECAST

ICEMA data shows FY25 sales at 1.40 lakh units (+3%), with Q1 FY26 already indicating +5% growth. Pepagora’s outlook projects 8–12% growth in FY26 (1.51–1.57 lakh units) and 12–15% growth in FY27 (1.69–1.81 lakh units). Rising Tier-2 demand will require nearly 25% dealer network expansion to meet equipment needs.

MATERIALS OUTLOOK

Cement capacity stands at 650 MTPA, covering around 115% of FY27 demand, while steel production at 185 MT provides 105% coverage. However, eastern infrastructure corridors continue to face a 10–15% logistics premium, impacting overall project costs.

WHO WINS?

Large players like L and T and HCC leverage strong balance sheets exceeding fifty thousand crore to secure major rail EPC tenders, while global brands such as Sany and LiuGong benefit from tier two service networks and maintain steady availability of fifteen to twenty five ton excavator stock. Rental firms, with nearly forty five percent market penetration, strengthen their position by deploying compact equipment quickly to meet project demands. Overall, success depends on financial strength, service reach, and strategic equipment placement aligned with market needs.

EXPERT CALLS

Industry leaders see strong structural tailwinds. The ICEMA CEO notes that the CIE scheme, backed by the Ministry of Heavy Industries under Shri H. D. Kumaraswamy, cuts prototype costs by 30%, calling it transformational for equipment manufacturers. NAREDCO highlights that City Economic Regions (CERs) are well aligned with the Tier-2 residential boom. CBRE adds that CPSE REITs are expected to stabilize office yields in the 7.5–8.5% range, improving investor confidence.

Â

12-MONTH ACTION PLAN

In Q1 FY26, focus on bidding HAM highway projects enabled by the Risk Guarantee Fund. By Q2 FY26, prioritize securing CER-linked urban contracts. In Q3 FY26, build inventory in the 15–25T equipment range to meet rising Tier-2 demand. By Q4 FY26, execute CPSE REIT retrofit projects to capitalize on redevelopment momentum.

KEY TAKEAWAYS

A ₹12.2 lakh crore capex push is expected to drive 15–18% EPC order growth. The Risk Guarantee Fund revives HAM execution, while CPSE REITs unlock ₹50,000 crore in redevelopment opportunities. CERs will accelerate the Tier-2 growth cycle, supported by PMAY-U 2.0 sustaining EWS housing demand. The ₹200 crore CIE scheme strengthens import substitution, and equipment demand in FY26 is projected to achieve an 8–12% growth target